How do I get out of debt on a low income?

You might be feeling overwhelmed by debt, thinking it’s impossible to find a way out with your current financial constraints but trust me, there are many others like you who have successfully navigated this path and have achieved debt-free living. In short, to get out of debt on a low income focus on the following:

Start with creating a budget to manage income & expenses. Minimize costs by cutting non-essential spending. Prioritize paying high-interest debts first. Consider additional income sources like part-time jobs or freelance work. Lastly, seek debt counseling for personalized advice.

Firstly, let’s address the elephant in the room – the feeling of being overwhelmed by debt.

It can be suffocating and crippling at times. The unending cycle of bills and due dates can make one feel as if they’re drowning.

Yet, remember that admitting that there is a problem is always the first step toward its solution. So applaud yourself for acknowledging it and seeking ways to rectify it.

Just because your income isn’t sky-high doesn’t mean you can’t achieve financial freedom. Contrary to popular belief, low-income families too can become debt-free with some strategic planning and discipline.

Whether through money-saving ideas or negotiating with creditors, numerous solutions exist for those struggling with debt despite their limited earnings. So how exactly does one get out of debt on a low income?

Well, there isn’t a magic wand for it, rather, it’s more of a multifaceted approach involving budgeting tips and spending hacks primarily aimed at making the most out of every penny earned. From adopting the debt snowball method or considering getting a debt consolidation loan – each person’s journey is unique based upon individual circumstances.

But before we delve into details about these topics like negotiating with creditors or consulting credit counseling agencies. Keep in mind that while walking down this path may seem daunting initially, many have trodden down similar paths before successfully!

What is debt?

Let’s take a moment to clarify the concept of debt. You may have heard the term thrown around in a variety of contexts, but what does it truly mean?

Simply put, debt is money owed by one party, you, the debtor, to another party, known as the creditor. This might be a bank or other financial institution – or perhaps a friend who lent you some cash when times were tough.

Debts typically come with an agreed-upon repayment time frame and often include interest charges that accrue over time. It’s not unusual for low-income families to struggle with debt, in fact, they’re often hit hardest by it.

High cost of living expenses combined with low wages can lead many into a cycle of borrowing just to make ends meet. It becomes all too easy to rely on credit cards for everyday spending – but when the bill comes due and more than minimum payments aren’t possible, the debt begins to grow.

Overwhelmed by debt can feel like standing at the foot of an insurmountable mountain – especially when you’re trying to get out of debt on a low income. But remember – every mountain is climbed step by step.

There are plenty of money-saving ideas and spending hacks out there that can help make this journey less daunting. It’s all about knowing where to look and how best to manage your resources.

In situations like these wherein individuals are scarcely able to skew their budget towards paying off debts rather than meeting basic needs, negotiating with creditors could be one potential solution for providing some much-needed relief from accumulating interests or sky-rocketing monthly payments.

Ideally, we would all aim for a life devoid entirely of owing money, a debt-free living if you will, but realistically speaking achieving this isn’t always straightforward especially when dealing with limited means.

Fortunately, strategies do exist such as getting a debt consolidation loan or employing methods like the debt snowball method or its flip side – the potentially faster yet harder-hitting “debt avalanche” method which focuses on paying off higher-interest debts first.

For those unfamiliar with these techniques simply put; they involve making minimum payments on all your debts while putting any extra funds towards one particular outstanding amount (be it either your smallest in size under the snowball method or highest interest rate under the avalanche method) until paid off completely before moving onto next target in line.

Achieving financial freedom is not only about how much you earn, it’s also about how efficiently you manage what you have!

Despite being on low income don’t despair – there are avenues available such as credit counseling agencies who offer guidance towards navigating complicated financial situations and help chalk out effective budget tips tailored specifically towards your needs keeping in mind your ability & comfort level thereby assisting you successfully pay-off debts gradually over a period without severely impacting day-to-day living expenses.

How debt can be overwhelming?

The feeling of being enveloped by towering waves of debt can be sickening. It’s like an enormous gray cloud looming overhead, casting a dark shadow over everything you do.

For low-income families, this overwhelming sense of dread can be especially potent. Every paycheck is consumed almost before it arrives, gobbled up by bills and bare necessities, leaving nothing for emergencies or savings.

Debt might feel like a monster lurking in the corners of your life, but remember that it’s something many people face. You’re not alone in this struggle, millions are trying to navigate their way out of debt on a low income every day.

The good news is that there are proven methods to tackle this beast and come out victorious on the other side – shining brightly into the world of debt-free living. One way you might consider tackling your debt is through the snowball or avalanche method.

The debt snowball method encourages you to pay off smaller debts first and then move on to larger ones, gaining momentum as each bill is paid down. On the other hand, the debt avalanche method suggests paying down debts with higher interest rates first to reduce overall interest paid over time.

Both strategies have their merits and can help bring about a sense of control when feeling overwhelmed by debt.

Yet another course could be getting a debt consolidation loan or seeking aid from credit counseling agencies that offer specialized services for those struggling with high levels of indebtedness while earning minimal income.

Debt relief for low-income people often takes the form of negotiating payment plans with creditors or adjusting interest rates. While we’re on the topic, let’s not forget about all those budget tips and spending hacks floating around either – they really do make a difference!

One might consider carpooling instead of maintaining an expensive vehicle or meal planning to avoid costly last-minute take-out orders. Small money-saving ideas like these can accumulate significant savings over time.

This newly freed-up cash can then help accelerate your journey toward financial freedom as you pay off remaining debts faster. Remember too those parting ways with any feelings of shame associated with being in debt is crucial in this journey towards financial freedom – it’s simply not productive nor helpful when working towards your goal.

To get out from under – once and for all – so you no longer need to ask yourself “How do I get out of debt on my low income?”

You’re taking action now. Each step brings you closer to seeing clearer skies ahead.

Is it possible to get out of debt on a low income?

The million-dollar question looms: is it possible to get out of debt on a low income? Let me assure you, it’s not only possible, it’s manageable with the right tools and mindset.

You may feel as if you’re swimming against a strong current, but remember, even the mightiest rivers start as tiny streams. Overwhelmed by debt, many low-income families often surrender to despair and stop fighting back.

But you’re not alone in this journey. Many organizations provide debt relief for low-income people who are struggling with debt.

One of the most effective methods used for getting rid of debts is what we call the “debt snowball method”. The idea here is to focus on paying off your smallest debts first while making minimum payments on larger ones.

As each small debt gets paid off, the money that would have gone towards those debts can now be redirected toward tackling larger ones. It’s like building a snowball from a handful of snow, as it rolls down the hill, it gathers more snow and grows larger.

Techniques have their merits because your choice between them depends largely on which one keeps you motivated and consistent in working towards financial freedom.

If both methods seem daunting or unfeasible given your circumstances, do not fret!

There exist numerous other avenues through which one can navigate their way out of indebtedness even when income seems sparse. Among these options is getting a debt consolidation loan which essentially combines various high-interest loans into one loan usually at a lower interest rate.

This could significantly reduce your monthly payments making them more manageable thus alleviating some financial strain. Negotiating with creditors directly or via a credit counseling agency can also be beneficial especially when completely drowning in high-interest-rate loans or credit card debt.

These agencies are skilled at negotiating for lower interest rates and setting up payment plans that suit your budget better.

But equally crucial are habits centered around frugality such as using efficient budget tips and implementing money-saving ideas like spending hacks among others for everyday expenses such as groceries or bills – every little bit helps!

The goal here isn’t merely surviving through tough times, instead getting out of debt on a low income means striving towards an existence defined by self-sufficiency and resilience where every dollar earned has value.

Don’t let being overwhelmed by debt convince you that life will always be shackled by financial constraints. There are ways to get out of this seemingly bottomless pit even amidst limited resources.

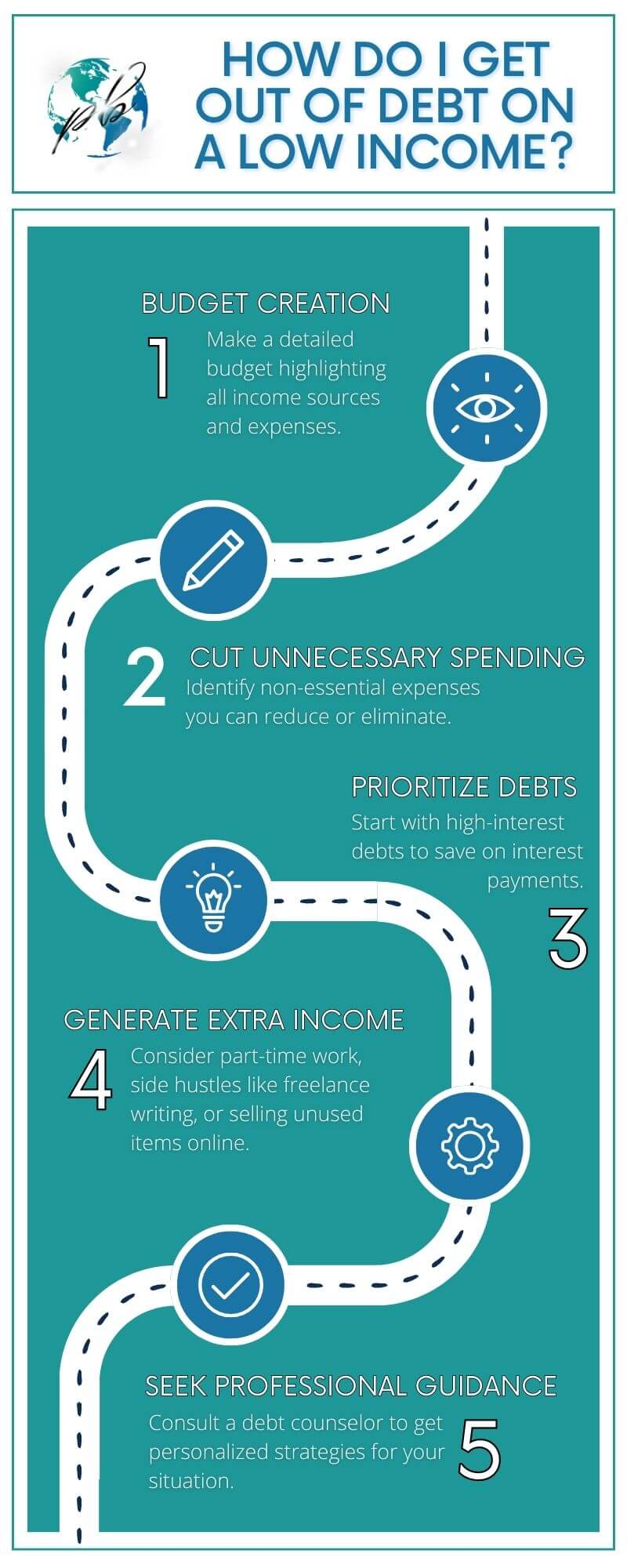

Step 1: Create a budget.

The journey to financial freedom begins with a simple yet powerful tool – a budget. Essentially, creating a budget is about understanding where your money comes from and where it goes.

It’s about being honest with yourself, knowing your income down to the last penny, and grasping all your expenses like rent or mortgage, utilities, groceries, transportation costs, and even those quick trips to the vending machine.

The idea is to get a clear picture of your financial situation as this will be key in determining how you can get out of debt on a low income. Now you might be thinking: “I’m overwhelmed by debt already. How could I possibly budget on such a low income?” That’s perfectly normal to feel that way.

But remember that even low-income families can work towards debt-free living through careful planning and some good old resilience. To start with the process of budgeting, first list down all your sources of income including full-time jobs, part-time gigs, or even side hustles if any are present.

Then document all your necessary expenses and any luxury items as well. You’d also want to account for variable costs such as gas and groceries which might fluctuate every month.

To help keep track of these spending habits there are many apps available online catering exactly for this purpose – these apps can become spending hacks in their own right. Once you’ve got everything listed down, it’s time for some serious reflection:

- Are there areas where you’re overspending?

- Can some unnecessary purchases be eliminated without affecting your quality of life?

- Do you see any opportunity for saving that wasn’t evident before?

Cutting back on non-essential expenditures is an important step toward achieving debt relief for low-income people. Negotiating with creditors may seem like an intimidating task but it can offer significant help when struggling with debt.

Whether it’s agreeing on lower interest rates or settling on minimum payments over extended periods, every little bit helps when trying to get out of debt on a low income.

The ultimate goal here is simple – spend less than what you earn so that the extra funds can be redirected towards paying off debts using either the debt snowball method or the debt avalanche method – two effective strategies often suggested by credit counseling agencies.

And finally while getting out of debt on a low income may seem overwhelming at first remember this – everyone’s journey to financial freedom looks different but one thing remains constant, perseverance pays off!

So don’t lose heart, instead brace yourself up for this journey through practical budget tips and money-saving ideas, believe me when I say that living free from debts is possible regardless of how steep the mountain ahead might seem.

Step 2: Cut your spending.

If you’re grappling with the weight of debt, especially on a low income, it can feel like a Herculean task to chip away at what you owe. However, with some strategic changes to your spending habits, it’s entirely possible to work towards financial freedom.

This isn’t about depriving yourself of everything you love but finding ways to stretch your dollars further and prioritizing where they go. Sometimes people are overwhelmed by debt because they don’t have a clear picture of where their money goes each month.

This is where spending hacks come into play. For instance, instead of buying coffee out every day which could cost $3-$5 per cup, why not make it at home for less than $1?

That’s already an extra few dollars saved per day which can pile up in the long run. Additionally, consider adopting principles from either the debt snowball method or the debt avalanche method as part of your strategy to cut down spending while paying off debts.

A common barrier for low-income families to become debt-free is high-cost bills like utilities or rent. One way around this is negotiating with creditors or service providers for better payment terms or lower rates – many are willing to discuss these options rather than lose a customer completely.

Another solution could be seeking help from a credit counseling agency that may provide budget tips and negotiate lower interest rates on your behalf. Another highly effective spending hack is shopping secondhand instead of new whenever possible – for clothes, furniture electronics, and more.

It’s also worth considering getting a debt consolidation loan which allows you to combine multiple owed amounts into one single loan often with lower interest rates making it easier and quicker for people striving for a life free from debt.

Money-saving ideas can come in various shapes. Maybe it’s carpooling or using public transportation instead of owning and maintaining an expensive vehicle, perhaps it’s cooking at home rather than eating out, maybe it’s canceling unneeded subscriptions; or possibly even downsizing your living space if feasible.

Cutting back on spending doesn’t mean giving up everything that brings joy – but rather re-evaluating wants versus needs and making intelligent choices accordingly. With effort and persistence, anyone struggling with debt can make strides toward becoming financially stable no matter their income.

Step 3: Choose a debt payoff method.

Getting out of debt on a low income may sometimes feel like trying to empty a bathtub with a teaspoon, but it’s not impossible.

I mentioned this before, but the best place to start is by choosing the right debt payoff method for your situation. Two popular methods often suggested by financial experts are the “debt avalanche” and “debt snowball” methods.

Now let’s dive into the nitty-gritty of these two approaches. Imagine you’re standing at the foot of an overwhelming mountain range – this is your debt.

The debt avalanche method involves targeting the highest interest rate debts first, just as you would tackle the tallest peak in that range first – hence avalanche. By focusing on these debts, you’ll save more money over time because you’re aiming to reduce what costs you most in interest. On the other hand, there’s also the debt snowball method made popular by financial guru Dave Ramsey.

This approach focuses instead on paying off your smallest debts first, regardless of interest rates. The logic behind this strategy is more psychological than mathematical: each small victory gives you confidence and momentum to keep going – just like how making a giant snowball starts with rolling up small amounts of snow.

However, if you’re overwhelmed by debt and both these methods seem daunting, there are other options for low-income families and individuals struggling with debt. One such alternative could be getting a debt consolidation loan.

This type of loan combines all your various debts into one single payment with a lower overall interest rate which makes it easier to manage and potentially pay off sooner. Connecting with a credit counseling agency is another way toward financial freedom when dealing with extensive obligations.

These agencies can provide valuable budget tips and money-saving ideas while also helping negotiate new payment plans or reductions in interest rates with creditors.

Always remember that while living under mountains of debt can be stressful and demoralizing, there are ways to get out from under it even on a low income – whether via strategies like utilizing spending hacks or attacking smaller bills first, focusing on high-interest debts, consolidating loans or seeking professional help from credit counseling agencies.

Every little step counts towards achieving that ultimate goal of debt-free living.

Step 4: Take additional steps to get out of debt.

So, what are these additional steps that could expedite your journey to financial freedom?

Well, it’s about time we dive into that.

The first action you could consider is getting a debt consolidation loan. This method helps to combine all your debts into one manageable payment.

You might find yourself asking which one is better for low-income families. The answer depends on your personal situation and mindset.

The snowball method involves paying off smaller debts first to gain momentum and a feeling of accomplishment. On the contrary, the avalanche method focuses on paying off debts with higher interest rates first, potentially saving you more money over time.

In addition, never underestimate the power of budget tips and spending hacks when living on a tight budget!

Little money-saving ideas can add up and make a significant difference in your ability to pay down debt faster.

For instance, you can cut back on eating out or cancel unused subscriptions – these small savings can supplement your repayments. If you feel overwhelmed by debt, remember; negotiating with creditors is also an option.

Many people struggling with debt are unaware that they can often negotiate lower interest rates or create a modified payment plan. Creditors are typically willing to negotiate as they would rather receive some payment than none at all.

But importantly, consider seeking professional help if needed from a credit counseling agency that specializes in providing effective strategies such as debt relief for low-income people trying hard to surf their way through this financial dilemma.

They provide assistance by reviewing your finances thoroughly and proposing options best suitable for you based on their expertise—remember not every solution fits everyone hence why expert advice can be priceless when it comes to achieving a life free from loans.

Remember that getting out of debt on a low income is indeed achievable, it requires persistence and determination!

Don’t let yourself succumb to despair or resignation, instead, embrace these helpful techniques and march defiantly towards a future of freedom—from every single penny owed!

Conclusion on how do I get out of debt on a low income.

Living within your means and managing to pay off debt on a low income may seem like an insurmountable task. It’s even more challenging for low-income families, who often struggle to make ends meet. However, with the right financial strategies and a little bit of discipline, it is indeed possible to achieve financial freedom.

The journey begins with understanding your expenses and creating a viable budget. Budget tips can be as simple as setting aside some money for emergencies or as complex as planning out each month’s expenses down to the last penny.

This will give you control over your finances and help you identify areas where you can save. Debt relief for low-income people often comes in the form of negotiating with creditors or seeking help from a credit counseling agency.

These organizations work with you to lower interest rates or monthly payments, making it easier to pay off what you owe. Another option could be getting a debt consolidation loan which allows you to combine all your debts into one manageable payment.

When it comes to paying off debts, two popular methods come to mind – the debt snowball method and the debt avalanche method. The former prioritizes paying off smaller debts first, which can motivate you by providing quick wins.

The latter focuses on eliminating higher-interest debts first, which can save more money in the long run.

However, getting out of debt on a low income also requires some creativity – finding money-saving ideas like spending hacks that reduce daily expenses, creating additional sources of income, or even downsizing your lifestyle temporarily might be necessary steps towards achieving that elusive debt-free living.

It’s easy to feel overwhelmed by debt but take heart that these difficulties are temporary bumps along your financial journey toward independence and security for yourself and your loved ones.

We all have different circumstances and challenges when dealing with our personal finances but remember – every step taken toward paying off that pesky loan is progress!

And before long those small steps become giant leaps until before you know it -you’re standing tall on the peak of financial security breathing in sighs of relief knowing well enough that indeed; yes -you can get out of debt on a low income!

FAQ about getting out of debt on a low income.

Words of encouragement on getting out of debt on a low income.

If you’re reading this, it means that you have already taken the first step toward setting yourself free from the shackles of debt. It’s not going to be a cakewalk, but let me reassure you, it is definitely achievable.

Remember, every journey begins with a single step and yours has just begun with understanding how to get out of debt on a low income. Do not let your spirit waver at the sight of overwhelming debt.

Many low-income families have been in your shoes and have successfully paved their path to financial freedom. They have managed to do so by employing various techniques such as getting a debt consolidation loan or using either the debt snowball or avalanche method.

These strategies may seem tough initially but are definitely manageable once broken down into small steps. If you are struggling with debt, remember that there are resources out there meant to provide you with support during these times.

Debt relief for low-income people is available through credit counseling agencies as well as through negotiating directly with your creditors. Asking for help does not portray weakness; rather it shows strength in recognizing when assistance is required.

Becoming overwhelmed by debt may sometimes feel like being stuck in quicksand—the more we struggle against it without a proper strategy, the deeper we sink into the financial quagmire.

But fret not!

There exists an array of budget tips and money-saving ideas at your disposal that can help steady your boat amidst this tempestuous storm called “debt”. These include spending hacks like learning how to differentiate between wants and needs, finding cheaper alternatives for expensive habits or items, and cutting back on non-essential expenses.

Always keep reminding yourself why you want this—to experience the joy of living a life free from constant worry about creditors, and to move towards securing a better life for yourself and your family, because everyone deserves peace of mind when it comes to finances.

The path toward financial freedom may be steeped in challenges but remember – every successful climb starts at the bottom and requires consistent effort coupled with determination.

You can pay off debt on a low income—it’s been done before—and quite soon enough you’ll find yourself standing atop that financial peak looking back at what once seemed an impossible uphill battle.

So go forth confidently on this journey toward achieving a state of debt-free living—a feat certainly attainable if armed with perseverance along with these insightful guidance points provided above.

Przemo Bania is a blogger and writer who helps people get out of their traditional jobs to start a blogging career. Przemo also runs a health blog advocating for endometriosis and fibromyalgia…