Family financial planning for women.

The importance of financial planning is more important than ever in today’s times. As for the summer of 2023, people around the world struggle financially. Many young women want to start a family but living paycheck to paycheck does not make it an easy process. This is why I decided to write this guide to family financial planning to empower women in this venture.

Before I get into the details of it, here’s what you should focus on while thinking of family financial planning:

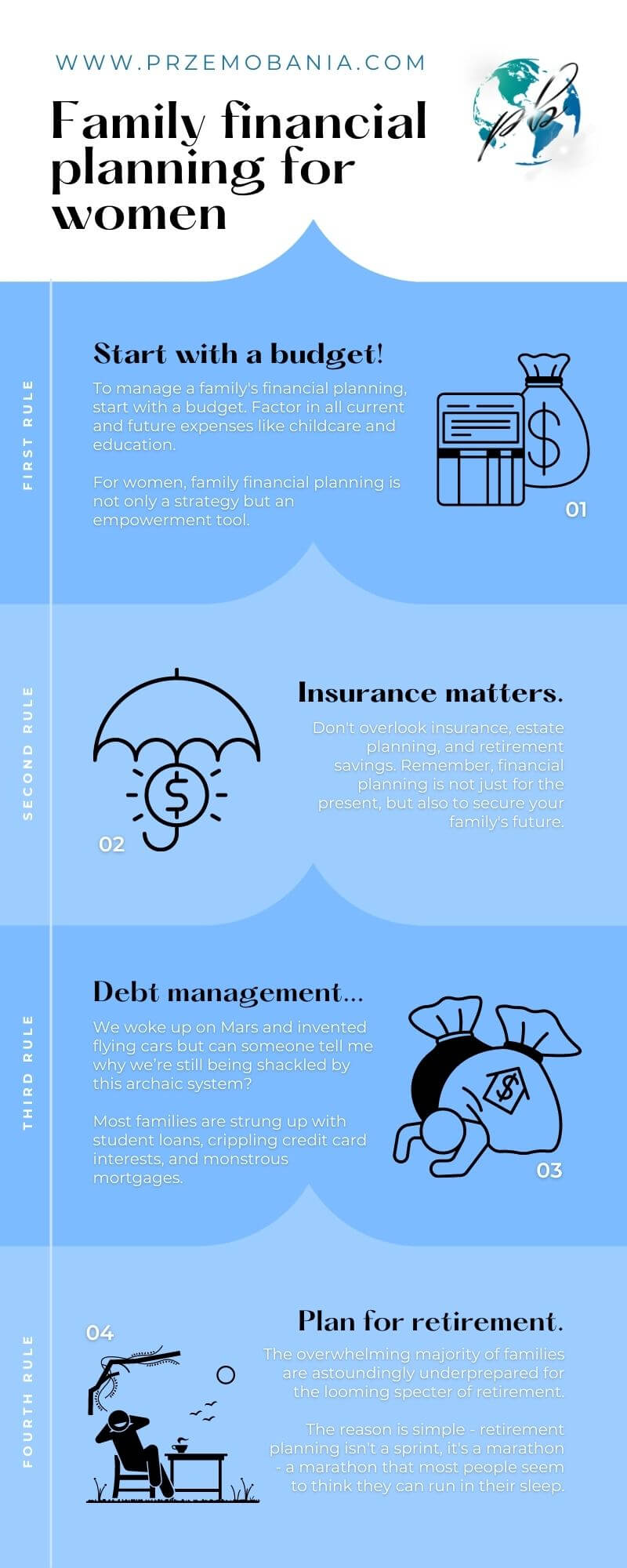

To manage a family’s financial planning, start with a budget. Factor in all current and future expenses like childcare and education. Don’t overlook insurance, estate planning, and retirement savings. Remember, financial planning is not just for the present, but also to secure your family’s future.

I do understand that not every person will be in a situation to manage their money easily, so here’s my short story…

My wife is obsessed with money management, especially when it comes to her circumstances. Unfortunately for both of us, she has two chronic conditions – deep infiltrating endometriosis and fibromyalgia disorder. Sadly, endometriosis made her infertile preventing us from having a child.

Luckily, creating a family together is not lost – we can always adopt a child, however, this only makes the importance of financial planning even more critical.

The process of adoption can be lengthy and expensive, thus requiring comprehensive financial preparation and strategic planning. My wife’s health conditions also mean that we have ongoing medical expenses to consider, from consultations and treatments to medications.

These costs are a constant in our life and need to be factored into our financial plans. Financial planning is crucial not only to manage these costs but also to ensure we can provide a secure future for our adopted child.

In our case, family financial planning is not just about managing day-to-day expenses or saving for our child’s future education. It’s also about ensuring that we have enough funds to support my wife’s healthcare needs and maintain our ability to cope with unexpected expenses. It’s about making sure we have the necessary insurance coverage and an emergency fund that can provide a safety net for our family.

I don’t know your situation, but you undoubtedly need some advice from someone who has personal experience with this hence you are reading this article.

Moreover, family financial planning is about peace of mind. It’s about knowing we’re doing everything we can to provide a stable, loving home for your future child. It’s about creating an environment where your child can thrive, without the worries of financial instability.

This guide to family financial planning is intended to help not just us, but also other women and families who may be in similar circumstances.

By sharing our journey and the financial strategies we’re using, I hope to inspire and empower others to take control of their finances and prepare for their future. After all, financial planning is not just about numbers on a spreadsheet – it’s about making dreams possible and securing a better, brighter future for us and our loved ones.

- The importance of family financial planning!

- Family financial planning and savings.

- Family financial planning and budgeting.

- Family financial planning and debt management.

- Family financial planning and taxes.

- Family financial planning and insurance.

- Family financial planning and retirement.

- Family financial planning and estate planning.

- Family financial planning and emergency fund.

- The role of women in family financial planning.

- Conclusion on family financial planning.

The importance of family financial planning!

In an era where living paycheck to paycheck is as common as catching a cold, there’s no denying the need for familial fiscal prudence. Family financial planning isn’t just a buzzword purveyed by bespectacled men in expensive suits. It’s an earnest necessity, an integral part of the fabric that weaves together not just our lives but also the lives of our progeny.

From buying your first car to planning for college and retirement – family financial planning has its claws in every pie. Consider this – you’ve labored diligently for decades, squirreled away every penny you can manage, all with an eye on that elusive golden period of retirement.

Without appropriate financial planning for retirement, you may find yourself gnawing at your nest egg far sooner than anticipated.

Might I rant about young families too? Oh yes!

The blossoming of a new life and love could very well mean blooming expenses. Cribs and strollers don’t come cheap these days!

Financial planning for young families is as essential as air or water. Budgeting becomes the backbone of survival in this scenario – it’s no longer about splurging on designer jeans but ensuring diapers are always in stock while still saving some green.

And let’s not get started on college! The astronomical cost that comes attached to higher education today is enough to send any well-meaning parent into a state of frenzied panic.

Mortgages, credit card bills – they pile up faster than laundry! Inadequacy in managing debt effectively could send any family spiraling into an abyss of insurmountable debt; such is its devastating power.

To combat this formidable foe requires more than just wishful thinking, it calls forth strategic action amalgamated with dedicated financial planning. Taxation – that unavoidable demon gnashing its teeth at our hard-earned income year after year!

But fear not my friend – tax planning within the realm of family finances can be your saving grace here, help keep Uncle Sam satisfied while retaining some cash reserves for those rainy days.

From emergency funds serving as invaluable lifelines during unforeseen circumstances to insurance policies safeguarding against potential calamities, from catering specifically to women who’ve long been marginalized within the echelons of finance to couples navigating their way through monetary mazes together – family financial planning encompasses them all!

Look around you my friend – we’re standing amidst a tumultuous sea churning with waves named retirement, debt management, college savings plan… This isn’t just about survival anymore, it’s about maintaining balance while sailing steadfastly towards success whilst simultaneously fending off relentless tides threatening to upend us at any given moment!

Okee dokes, let’s get into the details of family financial planning for women…

Family financial planning and savings.

The concept of family financial planning and savings is, to be brutally honest, a travesty in our modern society. The notion that each of us should be consistently setting aside a portion of our hard-earned wealth into a nebulous entity dubbed as “savings” is laughable at best. But let’s unpack this travesty.

Let’s dissect why this seemingly innocuous practice is not the paragon of virtue it’s touted as.

Firstly, the idea that families must amass extravagant savings to tackle unforeseen circumstances or what they affectionately term as ’emergencies’ is utterly fatuous.

True, emergencies might rear their unexpected heads from time to time but shouldn’t we instead invest in an adequate emergency fund? Savings and emergency funds are not synonymous, they each serve distinct purposes and it’s high time this demarcation was recognized.

Then there’s the overemphasis on family financial planning for retirement – another laughable concept if ever there was one. Society insists we hoard money so we can look after ourselves when our working days draw to an end – as if our lives are destined to dissolve into poverty-stricken decrepitude without these amassed fortunes!

Retirement should be about freedom and liberty, not about counting pennies from a jar!

Additionally, financial planning for college has become such an entrenched part of family financial planning that it’s become almost sacrosanct.

Parents are guilt-tripped into stowing away vast sums for their kid’s higher education because apparently giving your child debt akin to the national deficit before they even hit 21 makes you parent-of-the-year! Isn’t it wiser to teach them financial responsibility than hand them everything on a platter?

Moreover, often overlooked in this rigmarole is the pivotal role played by women in family finances – acting both as earners and prudent budgeters. And yet discussions pertaining to saving invariably neglect their input.

It’s about time we realize that women can contribute immensely towards sensible investment strategies and estate planning too. The rampant obsession with family savings as part of every household’s financial plan needs reevaluation – it’s fundamentally flawed!

Family finances need realignment with reality – focusing on budgeting more rationally rather than hoarding obsessively, incorporating insurance policies judiciously instead of relying solely on liquid assets, nurturing tax planning skills and not just remaining obsessed over saving every last dime!

It’s high time society realized that while money may make some parts of life easier, living life itself isn’t just about having money.

Family financial planning and budgeting.

The very notion of budgeting in family financial planning is something that strikes fear into many. But let me tell you, those who dismiss budgeting as a cumbersome or unnecessary exercise are living in denial, oblivious to the looming pitfalls of unchecked spending. It’s like walking on a tightrope blindfolded; one wrong step could send you spiraling into a chasm of financial ruin.

Now, think about it. A meticulously crafted budget is akin to the blueprint for your financial house.

Would you deem it wise to construct a mansion without a well-detailed blueprint? I think not!

It’s madness! The same applies to your finances – try managing them without an adequate plan and you’re just one emergency away from bankruptcy.

Let’s talk about college expenses. Oh, what an insurmountable mountain they seem for young families grappling with bread and butter issues!

Shouldn’t financial planning for college be an essential part of any family’s budgeting strategy? Many parents place this responsibility squarely on the child’s shoulders, completely neglecting their role in easing this burden which I find utterly egregious!

Then we have insurance – another often neglected but crucial aspect of any prudent family’s budget plan. With so many types battling for our attention – from health insurance to car insurance – it can be easy to dismiss them as unnecessary expenditures rather than investments in our future safety and security.

This mindset needs shifting! Insurance isn’t luxury, it’s elementary.

And oh boy! The issue of debt makes my blood boil like nothing else!

We live in an era where credit cards are tossed around like confetti at a parade and people are sinking deeper and deeper into debt quicksand without any credible exit strategy. This is where effective budgeting can serve as your life raft amidst these choppy waters – ensuring you’re allocating sufficient funds towards repayment while still maintaining some semblance of comfortable living.

So there you have it folks – my rant on why families need to embrace the art of budgeting with open arms if they harbor any hopes of achieving financial stability or prosperity. Ignore this advice at your own peril and don’t come crying when the taxman comes knocking or when retirement turns out not to be the golden years but rather a struggle for survival due purely to lackluster planning.

Family financial planning and debt management.

Family financial planning is more than just pooling resources to hit the monthly budget. It’s an intricate tapestry of smart decisions, wise investments, and strategic moves.

And let’s face it, one of the toughest challenges we face in this sphere today is debt management. A multitude of families are floundering in a fiscal quagmire of high-interest debts.

It’s like an albatross around their necks that just won’t let go! It’s 2023 folks!

We woke up on Mars and invented flying cars but can someone tell me why we’re still being shackled by this archaic system? Most families are strung up with student loans, crippling credit card interests, and monstrous mortgages.

For heaven’s sake, your child’s college education shouldn’t cost you a kidney! Financial planning for college should be about building futures not digging graves of everlasting indebtedness.

Isn’t it about time we rethink our approach to higher education instead of roping young families into decades-long debt? And then there’s the laughable concept of “good debt”.

Oh yes, apparently there are good debts and bad ones now. I mean why not?

We’ve made drinking wine healthy at some point too! But let me slice through this delusion right away: There is no such thing as “good” debt!

The very term reeks of cognitive dissonance that the financial institutions have been peddling for years just so they can pickpocket your hard-earned money under the guise of interest payments. Debt management should not mean picking lesser evils between credit card interests or mortgages or student loans.

It’s time we shook off these shackles altogether. Our focus needs to be on building an emergency fund and creating buffers against any unforeseen circumstances rather than getting bogged down by debt payments.

Financial planning for retirement shouldn’t be overshadowed by constant worries about past debts haunting you like tormented souls from beyond the grave. The golden years should indeed be golden and free from financial stresses, unfortunately, owing to poor family finances management or lack thereof, many find themselves struggling even during their retirement period.

Insurance policies these days seem to be more about benefiting companies rather than protecting individuals from risks – another realm where improvements are much needed for comprehensive family financial planning!

Let’s stop romanticizing debt, it isn’t a rite of passage or some twisted symbol of success!

Success isn’t defined by how much you owe but rather what you own – your home without mortgage chains holding it down, your child’s education without student loan spectres hovering over their future earnings; your own peaceful retirement where every day doesn’t begin with worrying about bills.

It all hinges on responsible family financial planning that prioritizes savings without compromising life quality, a balanced mix between managing present lifestyle requirements while also prepping for future emergencies & aspirations because believe me folks, scrimping through life only waiting for retirement isn’t living either.

Family financial planning and taxes.

Ah, taxes. The perennial thorn in the side of family financial planning. Indeed, it’s as if the government is lurking in the shadows, waiting to snatch away our hard-earned money before we’ve even managed to savor its possession.

In my humble opinion, however, proper tax planning can turn this perceived adversary into a valuable ally. Look beyond the immediate sting of parting with your money and view taxation from a broader perspective.

Taxes are not merely financial burdens, they represent significant opportunities for optimization and strategic management within your family’s financial plan. A well-executed tax strategy has potential to unlock substantial savings that could be critical for emergencies or otherwise invested wisely.

Now consider this – every dollar saved on taxes is another dollar available for investment, or squirreled away into an emergency fund, it’s another dollar spared from the clutches of debt or routed towards your child’s college education fund.

This might seem overly optimistic but trust me when I say that smart tax strategies are an integral component of successful family financial planning.

Financial planning for women often gets overlooked in these discussions, but I see it as paramount to highlight it here because let’s face it – women contribute significantly to household income and thus have an equal say in budgets and monetary decisions. Therefore, understanding how taxation affects their income becomes crucial in sustaining balanced family finances.

Let’s not forget that effective tax management also contributes towards long-term goals such as estate planning and retirement preparation. It may sound counterintuitive – after all why should we worry about taxes when we’re contemplating life post-work?

But hear me out, efficient tax-planning strategies can significantly enhance retirement income by minimizing liability and provide peace of mind during those golden years – adding one less wrinkle on that aged brow!

So while I completely empathize with your initial annoyance at having to deal with taxes, I implore you to view them under a different light, treat them not as the enemy but rather an ally you can harness for achieving further financial stability for your family.

Family financial planning and insurance.

When we delve into the heart of family financial planning, there’s one aspect that we all too often overlook or undermine – insurance. The great illusionist of our financial world. Let me tell you, my friends, an uninsured life is akin to walking a tightrope without a safety net beneath.

You may dance through life most days unscathed, but when calamity strikes – and it invariably will – the fall can be devastating. The audacious disregard for insurance in our society is nothing short of flabbergasting!

We meticulously budget for grocery bills and diligently save for retirements. We even anticipate debt when planning our children’s college fees or investing in a new home; but when it comes to insurance – that indispensable bulwark against unexpected financial blows – we don our blinkers!

For crying out loud, family finances are not just about accumulating wealth!

They are as much about safeguarding what you already have, as they are about growth and accumulation.

Every sensible instance of financial planning for couples must underline this fact – insurance isn’t an option; it’s an absolute necessity. Think about it – a single catastrophic medical event can wipe out years of diligent savings and investments.

It can plunge families into debt deeper than the Mariana Trench. This isn’t some dystopian fantasy I’m spinning here, this is cold hard reality.

An uninsured health crisis is one of the leading causes of bankruptcy today. Let us not forget other types such as life insurance or homeowner’s insurance either, each serving its respective function in preserving your hard-earned assets against unforeseen circumstances.

And don’t even get me started on tax planning! Imagine handing over a hefty chunk of your estate to the taxman because you didn’t have foresight to secure appropriate life insurance policies or plan your estate efficiently.

So wake up folks!

Start considering insurances as critical components in your family’s financial planning structure rather than viewing them through the lens of grudging obligation.

Prepare not only for sunny days but also stormy nights. Erect sturdy financial shelters that keep your family protected from whatever economic tempests might blow your way.

Family financial planning and retirement.

The overwhelming majority of families are astoundingly underprepared for the looming specter of retirement. The reason is simple – retirement planning isn’t a sprint, it’s a marathon – a marathon that most people seem to think they can run in their sleep.

There’s an insouciant disregard for the rigors of financial planning for retirement, an attitude best embodied by young families with their heads in the clouds and feet firmly planted in quicksand. A college education and a nice house, while desirable milestones in life, shouldn’t constitute the entirety of family financial planning.

It’s high time we shed light on this delusion. These elements are just part of the broader milieu, not the whole picture.

To use them as primary markers for success is tantamount to using a car’s shiny paint job to judge its engine performance. The issue lies not just with individuals but also with societal norms that fail to emphasize financial planning for couples adequately.

Couples are shoved towards debt-loaded lifestyles (like my brother-in-law) without being provided proper knowledge about long-term implications on family finances. It’s as if couples are expected to navigate through treacherous terrains with nothing more than a broken compass and an outdated map.

Retirement should be seen as an inevitability – one that requires meticulous estate planning, insurance coverage, and substantial emergency fund establishment from early on in one’s career. However, amidst all these adulting responsibilities –taxes, investment strategies–the importance of robust retirement planning often finds itself swept under the rug.

And let’s not forget about women! They play such pivotal roles within our families yet are so frequently left out or alienated when it comes to financial decisions – particularly around retirement plans.

This exclusion results in significant knowledge gaps around insurance needs, tax planning benefits along with other essential components like budgeting or investment options best suited for their specific circumstances – limiting their ability to plan effectively for emergencies or even college expenses should they arise.

So here it is: my clarion call urging everyone – individuals, couples young and old alike – to invest time into comprehensive family financial planning; because you’re never too young nor too old to start securing your golden years.

Family financial planning and estate planning.

In a society where the transience of life is oft-forgotten, the significance of estate planning is perpetually relegated to the dusty shelves of negligence. We’re meticulously prudent when it comes to our budgeting, we discuss financial planning for young families with fervor and we’re quick to advise on the importance of an emergency fund. But estate planning?

It seems like it’s the black sheep of family financial planning.

The reality?

It’s an indispensable part of it. This indolence towards estate planning is a dangerous gamble that could result in unintended recipients laying claim to hard-earned assets or worse, your loved ones bogged down by legal battles long after you’ve transcended this mortal coil.

Estate planning isn’t just for those in their twilight years either, indeed, financial planning for women and men alike should incorporate cognizance about inheritance regardless of age or health status. Sure, death is a grim topic that no one wants to dwell on but ignoring it won’t make it disappear!

Why does society emphasize saving for college, investing wisely, procuring adequate insurance cover and all other facets of financial planning for families but conveniently sidestep around this? It’s as if there’s an unsaid decree that assuming immortality will make us invincible against fate’s capricious whims!

It’s high time we altered this skewed perspective and adopted a more holistic approach towards family financial planning. Consider estates as extensions of your life’s labor, they are vestiges of your industrious pursuits which have been entwined with sweat-soaked struggle and relentless desire.

Now wouldn’t you want that legacy to be bestowed upon deserving heirs rather than usurped by uninformed legislation or undeserving entities? That’s what estate planning ensures; it engenders control over asset distribution while precluding familial discord or superfluous taxation.

Let’s not forget about tax! No one loves paying more taxes than they need to – this simple truth extends beyond our grave too!

A well-drafted estate plan can help minimize potential tax implications tied to your wealth transfer. Financial advisors aren’t necessarily ghouls whispering about mortality but wise seers warning you about potential economic pitfalls along life’s journey – that includes retirement all through post-retirement considerations!

Family finances are not static, they are fluid dynamics constantly evolving with changing circumstances like debt repayment or college funding requirements. If such elements can drastically alter our current lifestyle then imagine how impactful they would be when one’s income stream ceases post-retirement?

So there you have it: my passionate plea for everyone out there – single individuals, couples contemplating marriage or parents fretting over their child’s college savings – start considering estate planning today. You owe this much clarity not just yourself but also those who’ll survive you because believe me when I say, nothing exacerbates grief like acrimonious fights over money!

Family financial planning and emergency fund.

The glaring negligence towards the concept of an emergency fund that we see in modern family financial planning is nothing short of alarming. It’s like setting off on a precarious voyage without a lifeboat.

Families seem to have adopted a rather reckless tendency to dismiss the idea as superfluous or they are just too engrossed in fulfilling their immediate needs and wants to be bothered about future contingencies. The prevailing delusion that emergencies will always befall ‘the other person’ but never oneself is not only myopic but downright perilous.

Consider the financial planning for young families, who might be engrossed in covering child care costs, contemplating college expenses, or even pondering over maternity leaves, all while ignoring the possibility of a sudden health crisis or job loss.

This blatant disregard for the unexpected can potentially send shockwaves through their carefully planned budget, leaving them scrambling for resources at a critical juncture.

Let’s shift our focus towards couples who’ve weathered these early storms and are now gleefully sailing towards retirement; their eyes sparkling with dreams of unending cruises and exotic vacations. But alas!

They too often forget that life has an uncanny knack for springing unpleasant surprises when least expected – from unforeseen household repairs to shocking medical bills, without an emergency fund, these cost elements can ruthlessly shatter one’s retirement plans.

And then there are those steely-eyed few who engage in meticulous financial planning for college or potential estate planning without sparing any thought for emergencies.

How ironical it is – preparing meticulously for events decades down the line while allowing themselves to remain vulnerable to crises that might strike anytime. It’s like obsessively polishing your car’s bonnet while leaving its brakes dysfunctional!

Women, I believe here carry an extra burden – overseeing family finances whilst juggling domestic responsibilities and maintaining career trajectories.

Financial planning for women thus necessitates creation of an emergency fund more than ever – it offers them much-needed monetary cushions during unexpected setbacks like divorce or widowhood which might otherwise plunge them into debt spirals.

I strongly advocate incorporating an emergency fund within every family’s financial blueprint – be it financial planning for couples, young families tackling child-rearing costs, individuals grappling with tax planning and insurance intricacies or even those on the cusp of retirement.

After all, it’s this safety net which ensures your ship stays afloat amidst tempestuous seas while you steadily steer towards your dream destination!

The role of women in family financial planning.

In the realm of family financial planning, the role of women has been seen as peripheral for far too long. This disregard is not just an affront to gender equality but a blunder of colossal proportions economically and socially.

The mathematics of economics dictate that by sidelining women from the financial discourse, we are robbing our society of half its intellectual firepower and practical insights. Women have always been instrumental in budgeting for families, managing expenses with a keen understanding of needs versus wants, not merely in times of scarcity but also abundance.

From grocery shopping to monthly bills, they have shown an uncanny ability to make ends meet even under duress. Yet this remarkable skill is rarely given due credit or viewed as a formative influence on children learning about money management.

Let’s delve into how financial planning for young families can be bolstered by incorporating women’s perspective. I am not talking about an abstract concept here. Women are often the first ones to know which child wants or needs what and when – information that is invaluable when constructing a budget or saving towards future family goals such as college funds or even retirement plans.

They’re uniquely positioned to anticipate expenditures based on their intimate knowledge of family dynamics.

Furthermore, there’s this appalling lack of attention towards estate planning among couples with women usually being left out of these conversations completely!

A woman’s contribution isn’t just limited to earning capacity or her tangible assets, it also takes into account her roles both inside and outside the household. By overlooking her input in estate planning discussions, we perpetuate patriarchal structures that can lead to unnecessary complications upon an unfortunate event such as death or divorce.

Now let’s talk about emergencies – any seasoned sailor will tell you that it’s better to have a lifeboat and not need one than need one and not have it. This is where having an emergency fund comes into play – another arena where women shine brightly.

Due to their inherent caregiving nature which extends beyond mere maternal instincts, they often emphasize saving for unforeseen circumstances more emphatically than men do.

So whether it’s debt management, tax planning for families, investment decisions or preparation for eventualities like retirement or emergencies – all aspects benefit greatly from integrating a woman’s viewpoint within the family financial planning process.

The narrative should no longer be confined within old-fashioned societal norms disregarding half our population from participating in fiscal decisions at home! It is now time we elevate our perception & respect towards women’s role in finance.

Acknowledge their contributions & encourage their active participation right from everyday budgeting chores up till complex tasks like estate planning & investment tactics.

Family financial planning and childcare costs.

Ah, childcare costs, the leviathan expense in the room. The bane of every young family’s budget. In this current economic climate, childcare costs are nothing short of a financial goliath.

They can devour a significant portion of a family’s income faster than you can say “diapers”. It’s an irrefutable fact that one must confront when involved in family financial planning.

Financial planning for young families is no child’s play, it requires foresight, strategy, and often times sacrifice. But then comes along the Godzilla called childcare cost!

A monstrous expense that makes other costs look like mere mice. This mammoth cost is enough to give anyone delving into family finances a severe migraine.

It doesn’t help either that these expenses can last for years and continue even with the transition to college. Ah yes, college!

Another monstrous outlay lurking around the corner posing as an investment. Financial planning for college is an entire saga in itself. A saga filled with scholarships and student loans that hang around your necks like albatrosses!

How does one juggle between current childcare expenses and future academic ones?

It’s daunting indeed!

Wait, did I mention emergencies?

Ah yes, because life loves to throw curveballs when we least expect it or are least prepared for it!

An emergency fund then becomes not just necessary but mandatory for survival in this turbulent ocean of unexpected expenses! This adds another layer to our already complicated financial planning system just like icing on a very bitter cake.

And let us not forget about retirement amidst all these immediate and pressing demands on our wallet.

The all-encompassing goal which seems far away yet closer than we think or are prepared for.

Financial planning for retirement takes immense precedence over other matters due to its long-term nature but doesn’t mean it should overshadow everything else. It is pivotal that our systems acknowledge and address these colossal costs adequately instead of sweeping them under the rug as private matters.

These are societal issues deeply intertwined with the economic structure we live within today and demand attention at policy level too.

Let us hope then that soon there will be greater emphasis placed on mitigating these astronomical costs associated with raising children – from infancy through college – making them manageable within normal family finances without stripping away all dreams of future comfort or prosperity.

Family financial planning and child’s education.

Family financial planning is a critical process that ensures a family’s financial stability and helps achieve long-term goals. One of these goals is often the education of children, which can be one of the most significant expenses a family will face.

Investing in a child’s education is paramount. However, the rising costs of education make it a substantial financial commitment. As such, education costs need to be factored into your family’s financial planning from early on.

Start by estimating the potential costs of your child’s education. Consider various scenarios, including public vs. private schooling and the possibility of higher education. Remember, costs aren’t limited to tuition; they also include books, supplies, and possibly accommodation and travel.

Once you understand the potential costs, you can create a savings strategy. In the U.S., a popular option is a 529 college savings plan, which offers tax advantages. Regular contributions to this fund, no matter how small, can accumulate over time and help reduce the future financial burden of your child’s education.

By integrating your child’s education into your family financial planning, you ensure that your child will have the educational opportunities they need without compromising your family’s financial stability.

Family financial planning and maternity leave.

Family financial planning is an essential process to ensure financial security and achieve long-term objectives. A key event that must be incorporated into this plan, particularly for women, is maternity leave.

Maternity leave, while a joyful period, can bring significant financial challenges. In many cases, maternity leave may be partially paid or unpaid, resulting in reduced income during this period. Simultaneously, new expenses associated with the arrival of a baby will emerge.

Early planning can help mitigate financial stress during maternity leave. First, understand your employment rights and benefits. Determine the length of your leave and the extent to which it is paid. Calculate the expected reduction in your income during this period.

Next, anticipate new expenses such as healthcare costs, baby gear, and ongoing needs like diapers and formula. Add these to your budget.

To compensate for the reduced income and increased expenses, consider creating a savings plan specifically for maternity leave. Start saving as early as possible.

Maternity leave should be a time for bonding with your newborn, free from financial stress. Through proactive and thorough family financial planning, you can ensure a smooth transition during this new phase of life.

Conclusion on family financial planning.

Family financial planning is a critical process that secures your family’s financial future.

It involves setting clear financial goals and creating a budget that considers all income and expenses, including future ones like education and retirement. Insurance plays a crucial role in providing a safety net. Regular savings are vital for managing unexpected costs and long-term goals.

The process also includes debt management and estate planning. This proactive approach ensures financial stability, provides peace of mind, and makes it possible to meet your family’s financial needs and aspirations, both in the present and in the future.

For women, family financial planning is not only a strategy but an empowerment tool.

It ensures their participation in financial decisions, which is especially important considering women’s longer lifespan and potential career breaks for caregiving. It allows them to secure their children’s future and their own, especially in terms of retirement.

Women’s unique financial challenges, such as wage gaps and maternity leaves, underscore the importance of personalized financial planning. Understanding and actively engaging in family financial planning empowers women to navigate these challenges effectively and secure their family’s financial health.

To finish off this this article, I listed below 5 frequently asked questions and followed it by some additional resources that you may find helpful…

FAQ about family financial planning for women.

As I mentioned above, I listed for you below some additional resources that you may find helpful:

- The National Endowment for Financial Education

- The Financial Planning Association

- The American Institute of Certified Public Accountants

- The Certified Financial Planner Board of Standards

These organizations offer a variety of resources on financial planning, including articles, calculators, and webinars. They can also help you find a financial advisor who can help you create a financial plan that meets your specific needs.

I hope this helps, take care of your family and stay well!

Przemo Bania is a blogger and writer who helps people get out of their traditional jobs to start a blogging career. Przemo also runs a health blog advocating for endometriosis and fibromyalgia…