Steps in financial planning.

Every person has a different reason to take an interest in their financial situation, but what most of us have in common is the constant struggle to make ends meet. The reasons why I decided to write about “steps in financial planning” came also out of necessity, although I am, indeed, obsessed with the topic of personal finance.

Life often schools us in unexpected ways.

Growing up in the ’80s in Poland under the shadow of Russian communism, my meals often consisted of just bread and drippings. Those stark memories shaped my understanding of life’s hardships. Yet, it was my wife’s chronic conditions that truly opened my eyes to the emotional, mental, and especially financial struggles of life.

Our challenges weren’t found in textbooks. They reminded me of the glaring gaps in our education system, which often equips us for jobs but leaves us floundering in the real world of money and personal finance.

Drawing from my childhood resilience and the wisdom I’ve absorbed from countless books and invaluable insights from my accountant twin brother, I’ve embarked on a mission. My passion for personal finance, blogging, and platforms like Pinterest isn’t just for the sake of it. It’s a fervent desire to help others, especially those grinding away, paycheck to paycheck, seeking solace in a sea of financial chaos.

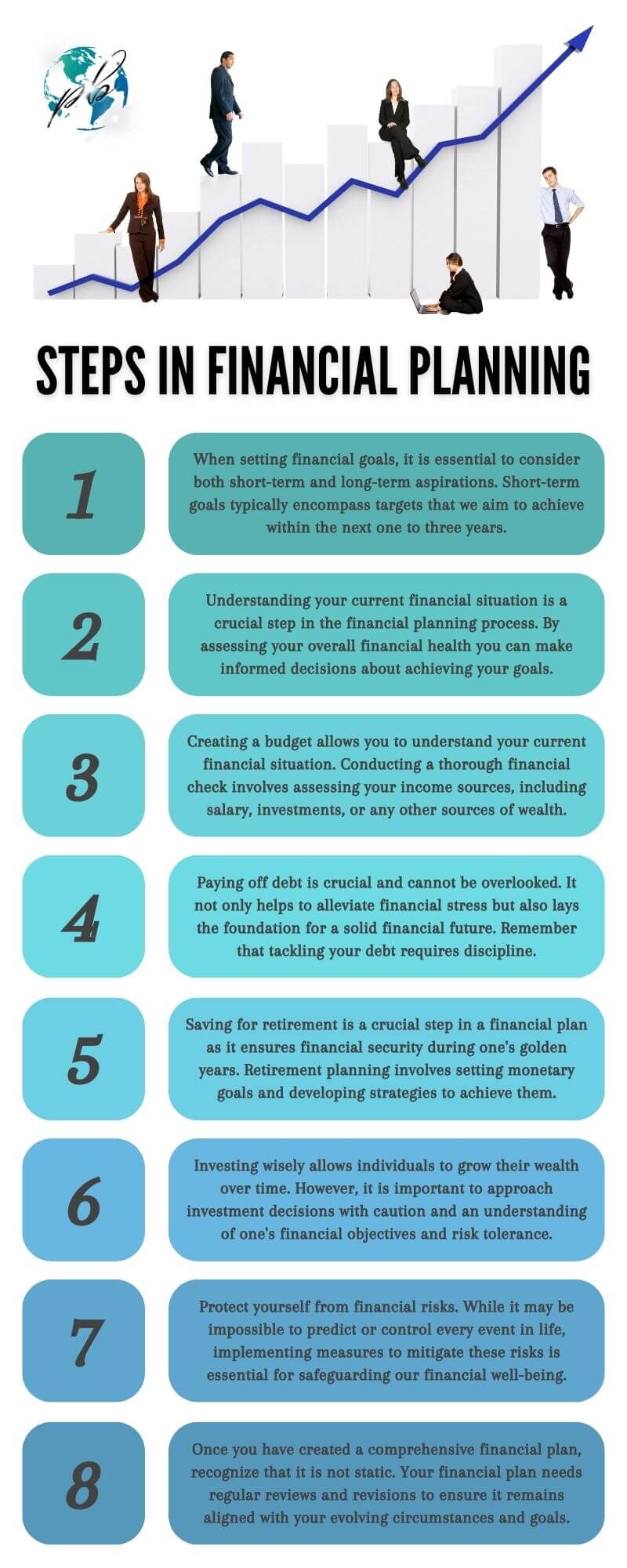

Steps in financial planning focus on many areas, including setting financial goals, understanding your current financial situation, creating a budget, paying off debt, saving for retirement, investing wisely, protecting yourself from financial risk, and reviewing and revising your plan regularly.

Let me share with you not just steps in financial planning, but a roadmap crafted from personal experience and genuine care. You’re not alone on this journey, and together, we can navigate toward a more secure financial future.

8 steps in financial planning.

Navigating life’s complexities without a plan is akin to setting sail without a compass. Financial planning is that vital compass for your monetary journey.

By outlining clear steps, it demystifies the path to achieving both short-term needs and long-term aspirations. It equips you with the foresight to anticipate challenges, make informed decisions, and build a resilient future. Embracing these steps not only secures your financial well-being but also instills a profound sense of empowerment and confidence in steering the course of your life.

Before I dive in to help you understand the unparalleled importance of steps in financial planning, here is what we are going to discuss one by one how to:

- Set financial goals.

- Understand your current financial situation.

- Create a budget.

- Pay off debt.

- Save for retirement.

- Invest wisely.

- Protect yourself from financial risks.

- Review and revise your plan regularly.

Set financial goals.

Setting financial goals is a crucial first step in the journey towards achieving financial independence and securing a bright future. Without clear objectives, it becomes challenging to create a roadmap that will guide our financial decisions and actions. By setting tangible monetary goals, we establish targets to strive for, enabling us to make more informed choices regarding saving, investing, spending, and debt management.

When setting financial goals, it is essential to consider both short-term and long-term aspirations. Short-term goals typically encompass targets that we aim to achieve within the next one to three years.

These may include saving for a vacation or paying off high-interest debt. On the other hand, long-term goals revolve around milestones we hope to reach in five years or more—such as buying a house or retiring comfortably.

To effectively set financial goals, it is important first to conduct an honest assessment of our current financial situation. We should evaluate our income, expenses, assets, liabilities, and overall financial health.

This self-awareness helps us establish realistic and attainable objectives that align with our capabilities and resources. Once we have assessed our current standing and identified our short-term and long-term objectives, the next step is prioritization.

It is essential to determine which goals are most important or urgent so that we can allocate resources accordingly. For example, if we have significant high-interest debt obligations weighing us down financially, it may be wise to prioritize paying off those debts before allocating funds towards other long-term investments.

An effective strategy for goal-setting involves ensuring they are specific, measurable actionable relevant time-bound (SMART). By making each goal specific—for instance: “Save $10k for an emergency fund within two years” — we provide ourselves with clarity on what exactly needs to be achieved.

Measurability ensures that progress can be tracked over time using quantifiable metrics such as savings account balance or net worth. Moreover,having actionable steps allows us to break down complex targets into smaller, manageable tasks.

This makes our financial goals less intimidating and increases the likelihood of success. Additionally, ensuring that our goals are relevant to our overall financial objectives and align with our values and aspirations reinforces our motivation to achieve them.

Incorporating a time-bound element into setting financial goals provides a sense of urgency and accountability. By establishing specific timelines within which we aim to attain each goal, we create a framework for regular evaluation and adjustment of our progress.

This enables us to track how well we are adhering to the steps in our financial planning journey. Setting financial goals is an essential component of designing a comprehensive financial plan.

By evaluating our current situation, identifying both short-term and long-term objectives, prioritizing effectively, applying the SMART framework, and establishing time-bound targets, we lay the foundation for making informed decisions regarding saving, investing, debt management, insurance coverage, and ultimately achieving financial independence.

Seeking guidance from a qualified financial advisor can also be invaluable in this process as they can provide expertise in areas like risk assessment or investment strategies while helping us navigate the steps in financial planning with greater confidence and clarity.

Understand your current financial situation.

Understanding your current financial situation is a crucial step in the financial planning process. By assessing your overall financial health, you gain clarity on where you stand and can make informed decisions about achieving your monetary goals.

This section will provide a comprehensive guide to understanding your current financial situation, encompassing various aspects such as net worth calculation, debt management, and asset allocation.

To begin this process, it is important to conduct a thorough evaluation of your personal finance. One vital aspect is determining your net worth, which involves calculating the difference between your total assets and liabilities.

This assessment provides an accurate snapshot of your current financial standing and helps establish a baseline for future progress. Additionally, examining cash flow patterns and monthly expenses allows you to evaluate how effectively you are managing income and expenses.

Debt management is another critical component of understanding your financial situation. Evaluate all outstanding debts – including credit card debts, loans, or mortgages – by analyzing interest rates, payment terms, and outstanding balances.

By doing so, you can identify opportunities for consolidation or refinancing that may help save money in the long run. Furthermore, it is essential to consider both short-term and long-term goals when assessing your current financial situation.

Short-term goals may include building an emergency fund or saving for a specific purchase within the next few years. Long-term goals might involve retirement savings or wealth accumulation for future financial independence.

As part of understanding your personal finance better, it is advisable to review any existing investments or investment strategies you have employed thus far. Analyze the performance of various financial instruments in which you have invested – such as stocks or bonds – along with their associated risks and returns.

Consider whether these investments align with your overall financial goals and if adjustments need to be made in terms of asset allocation or portfolio management. While conducting this assessment independently can be beneficial, seeking guidance from a qualified professional like a fiduciary advisor can provide invaluable insights into optimizing your finances.

A trusted financial advisor can help analyze your financial situation holistically, offering expert advice on investment strategies, risk management, and setting realistic financial milestones. Understanding your current financial situation is an integral part of the overall steps in personal financial planning.

By conducting a comprehensive evaluation that includes net worth calculation, debt management, goal setting, investment strategy review, and seeking professional guidance when needed, you pave the way for sound decision-making and effective wealth management.

This thorough assessment ensures a strong foundation for future financial planning endeavors while striving towards achieving your long-term financial goals.

Create a budget.

Creating a budget is an integral part of the financial planning process. It provides a roadmap for managing your income and expenses, helping you make informed decisions about your monetary position and achieve your financial goals. In this section, we will delve into the importance of creating a budget, steps to develop one, and strategies to maintain its effectiveness.

To begin with, creating a budget allows you to gain a comprehensive understanding of your current financial situation. Conducting a thorough financial health check involves assessing your income sources, including salary, investments, or any other sources of wealth accumulation.

Simultaneously, it entails evaluating your expenses across various categories such as housing costs, transportation expenses, debt repayments, insurance premiums, and discretionary spending.

Once you have collected all the necessary data for your financial review, it’s time to proceed with developing the budget itself.

Start by categorizing your income and expenses into fixed costs (such as rent/mortgage payments or insurance premiums), variable costs (like utility bills or grocery expenses), and discretionary costs (such as entertainment or dining out).

This step enables you to identify areas where you can potentially cut back on expenditures or reallocate funds towards more pressing goals.

With the categorization complete, it is crucial to allocate realistic amounts for each category based on past spending patterns while considering future aspirations. Setting limits within each category will help prevent overspending and ensure that your financial forecast aligns with long-term goals.

Be mindful of any irregular expenses that may arise sporadically throughout the year (e.g., car maintenance or medical bills) by including an allocation for these in your budget. Savings should also be an essential component of any well-structured budget.

Set aside a designated portion of your income specifically for savings purposes—an amount that suits both short-term needs (e.g., emergency fund) as well as long-term objectives like retirement savings or investment plans. Incorporating regular contributions towards these goals ensures that they are not neglected amidst daily expenses and help you stay on track with your financial roadmap.

Maintaining the effectiveness of your budget requires regular monitoring and periodic adjustments. Regularly review your budget to assess whether you are staying within the allocated limits for each category.

Consider conducting a financial review every few months or annually to evaluate changes in your financial circumstances, reassess your goals, and make necessary modifications to optimize your budget.

Creating a well-structured budget is an essential step in personal financial planning.

It provides a framework for managing income and expenses while ensuring progress toward long-term goals.

By conducting a thorough assessment of your monetary position, categorizing expenses diligently, setting realistic limits, prioritizing savings, and regularly reviewing and adjusting the budget as needed, you can take control of your finances and increase your chances of achieving financial health and stability.

Pay off debt.

Paying off debt is a crucial step in financial planning that cannot be overlooked. It not only helps to alleviate financial stress but also lays the foundation for a solid financial future. Whether it’s credit card debt, student loans, or any other form of borrowing, tackling debt requires discipline and strategic decision-making.

One approach to paying off debt is the snowball method. This technique involves listing all your debts from smallest to largest and focusing on paying off the smallest debt first while making minimum payments on other debts.

Once the smallest debt is paid off, you move on to the next smallest one, and so on. This method provides a psychological boost as you see progress being made and helps build momentum toward eliminating larger debts.

Another approach is the avalanche method, which prioritizes tackling higher-interest debts first. By focusing on high-interest debts like credit cards or personal loans with exorbitant interest rates, you can save money in the long run.

This method may not provide instant gratification like the snowball method, but it ensures that you make more efficient use of your resources by minimizing interest payments. It’s worth noting that before embarking on a debt repayment plan, conducting a thorough financial health check is essential.

Analyze your income sources, expenses, and other financial obligations to determine how much you can allocate toward debt repayment each month without compromising your ability to meet essential needs or saving for emergencies. Additionally, exploring options like refinancing or consolidating your debts can be beneficial in certain situations.

If you have multiple high-interest-rate loans or credit card balances scattered across various accounts, consolidating them into one manageable loan with a lower interest rate can simplify your finances and potentially reduce monthly payments. In conjunction with paying off debt, it’s crucial to resist accumulating new liabilities during this process.

Sticking to a budget will help curb unnecessary spending and ensure that money is directed toward repaying existing debts rather than accumulating new ones.

Overall, paying off debt is a significant step in financial planning that requires careful consideration and strategic decision-making.

By employing methods like the snowball or avalanche approach, conducting a financial health check, exploring refinancing options, and maintaining a disciplined approach to spending, you can work towards achieving financial independence and laying the groundwork for long-term wealth management.

Remember, seeking guidance from a fiduciary or qualified financial planner can provide valuable insights tailored to your specific financial goals and aspirations.

Save for retirement.

Saving for retirement is a crucial step in financial planning, as it ensures financial security during one’s golden years.

As we age, our ability to work and earn income may diminish, making it essential to accumulate a sufficient nest egg to cover expenses and maintain a desirable lifestyle. Retirement planning involves setting monetary goals and developing strategies to achieve them, which can be facilitated by seeking guidance from a financial planner who specializes in retirement savings.

One of the first considerations in saving for retirement is determining your financial aspirations and the lifestyle you envision during your post-working years. Understanding your desired standard of living will help you estimate the amount of money required to sustain it.

A financial planner can assist in this process by conducting a thorough analysis of your current monetary position, including net worth calculations, income streams, expenses, and investments.

Once you have established your retirement goals, developing an effective savings plan becomes paramount.

Budgeting plays an integral role here – by tracking and controlling spending habits, individuals can allocate funds towards their long-term planning objectives. With the assistance of a financial planner, you can identify areas where adjustments can be made to free up additional cash flow for retirement savings.

An essential aspect of saving for retirement is determining an appropriate asset allocation strategy. This entails diversifying investments across different asset classes with varying levels of risk and return potential.

While younger individuals may generally tolerate more risk given their longer investment horizon, those nearing retirement age tend to prefer more conservative approaches that prioritize capital preservation over capital growth.

Retirement planning also involves considering potential risks that could impact one’s monetary situation later in life.

Adequate insurance coverage can protect individuals from unforeseen events such as disability or illness that might hinder their ability to work or accrue income during their working years or even after retiring. Saving for retirement is a vital step in the overall process of financial planning.

It requires careful consideration of one’s future aspirations, budgeting strategies, asset allocation plans, and risk-management measures. Seeking the guidance of a knowledgeable financial planner can ensure that you are on track to meet your retirement goals while providing peace of mind about your financial future.

Invest wisely.

Investing wisely is a crucial step in financial planning that allows individuals to grow their wealth over time. However, it is important to approach investment decisions with caution and an understanding of one’s financial objectives and risk tolerance.

By making informed choices, individuals can maximize their returns and work towards achieving their long-term goals. One of the first considerations when investing wisely is to determine the appropriate asset allocation for your portfolio.

This involves diversifying investments across different asset classes such as stocks, bonds, real estate, and commodities. The allocation should be tailored to your financial goals, risk tolerance, and time horizon.

A financial planner can provide valuable guidance in creating a well-balanced portfolio that suits your monetary position. In addition to asset allocation, it is essential to conduct thorough research before investing in specific securities or funds.

This involves analyzing the historical performance of potential investments, understanding their underlying assets or businesses, and evaluating their future prospects. Conducting a risk assessment helps in determining the level of volatility associated with various investments and guides decision-making accordingly.

Investors should also consider the benefits of long-term planning when making investment decisions. Instead of trying to time the market or chasing short-term gains, a disciplined approach focusing on long-term wealth accumulation often yields superior results.

This strategy allows individuals to ride out market fluctuations and benefit from compounding returns over extended periods. Another aspect of investing wisely is regularly reviewing and rebalancing your portfolio.

As life circumstances change or market conditions shift, it may be necessary to adjust your asset allocation or sell certain holdings that no longer align with your financial objectives. Regularly monitoring your investments ensures that you stay on track towards achieving financial independence.

While seeking professional advice from a financial planner can be beneficial at every step in financial planning, it holds particular importance when it comes to investing wisely. A qualified professional can provide personalized guidance based on your unique circumstances and help you navigate complex financial markets.

They can also assist with wealth and portfolio management to ensure that your investments are aligned with your long-term goals. Investing wisely is a critical step in financial planning that requires careful consideration of one’s financial goals, risk tolerance, and time horizon.

By diversifying assets, conducting thorough research, adopting a long-term approach, regularly reviewing and adjusting portfolios, and seeking professional advice when necessary, individuals can position themselves for success in the investment arena.

Taking these steps not only enhances one’s financial health but also paves the way towards achieving their financial aspirations.

Protect yourself from financial risks.

In the realm of personal finance, protecting oneself from potential financial risks is a crucial step toward maintaining long-term financial health.

While it may be impossible to predict or control every unexpected event that life throws our way, implementing measures to mitigate these risks is essential for safeguarding our financial well-being. Adopt prudential strategies and seek professional guidance when necessary so you can fortify your monetary position and ensure greater stability.

One of the first aspects to consider when protecting yourself from financial risks is having adequate insurance coverage.

Insurance serves as a safety net by providing protection against unforeseen circumstances such as accidents, illnesses, property damage, or even loss of income.

Evaluating your specific needs based on factors like age, health condition, dependents, and overall financial objectives will enable you to make informed decisions about which types of insurance are most appropriate for you. This could include health insurance for medical expenses or disability insurance in case of an accident or injury that prevents you from working.

Additionally, tax planning is another avenue through which individuals can minimize financial risk exposure. Collaborating with a knowledgeable financial advisor who specializes in tax matters helps in optimizing your tax strategy while remaining compliant with legal requirements.

By taking advantage of tax deductions and credits available in your country or region, you can reduce your taxable income and potentially increase your savings. Building an emergency fund acts as another line of defense against unexpected events that can impact one’s financial stability.

An emergency fund represents a reserve specifically set aside to cover unforeseen expenses such as medical emergencies or sudden unemployment.

Aim to accumulate three to six months’ worth of living expenses in this fund so that you have enough liquidity to weather any temporary setbacks without compromising your long-term savings goals.

Diversification plays a vital role in shielding yourself from market-related risks and achieving long-term wealth accumulation objectives across different asset classes. By spreading investments among various types of assets (stocks, bonds, real estate, etc.) and sectors, you reduce the likelihood of significant losses due to the underperformance of a single investment.

Regularly reviewing and rebalancing your portfolio with the help of a financial advisor ensures that your investment strategy aligns with your risk tolerance and financial milestones. Maintaining financial literacy is key to protecting oneself from potential risks.

Staying informed about personal finance concepts and trends enables you to make sound decisions regarding investments, insurance coverage, or even seeking professional advice. Expanding your knowledge through books, online resources, or attending financial workshops equips you with the necessary tools to assess risks accurately and make informed choices.

Protecting yourself from financial risks is an integral part of sound financial planning.

By proactively addressing potential vulnerabilities through insurance coverage, tax planning strategies, emergency funds, diversified investments, and ongoing education in personal finance matters; individuals can ensure greater stability in their monetary journey.

Seeking guidance from a qualified financial advisor can also provide invaluable insights tailored to your specific circumstances and goals. Ultimately, taking these steps towards protecting yourself against potential risks now will contribute significantly to achieving long-term financial independence.

Review and revise your plan regularly.

Once you have created a comprehensive financial plan, it is crucial to recognize that it is not a static document. Your financial plan needs regular reviews and revisions to ensure it remains aligned with your evolving circumstances and goals.

By engaging in periodic evaluations, you can make necessary adjustments and stay on track towards achieving your financial aspirations. Regularly reviewing your plan provides an opportunity to assess the progress you have made towards your monetary goals.

It allows you to evaluate whether you are staying within budget, saving enough, and making appropriate investments.

During this process, it may be beneficial to consult with a financial advisor or planner who can offer expertise and guidance based on their knowledge of current market trends and insights.

A crucial aspect of the review process is assessing changes in your financial situation.

Life events such as getting married, having children, changing jobs, or receiving an inheritance can substantially impact your long-term planning needs.

By conducting regular reviews, you can adjust your plan accordingly to accommodate these shifts in circumstances. Portfolio management is another critical consideration during the review stage.

Assessing the performance of your investments allows you to determine whether they are meeting expectations or if adjustments need to be made. Diversification should also be evaluated regularly to ensure that risk is appropriately spread across different asset classes.

Reviewing insurance coverage is essential for protecting yourself from potential financial risks. As part of the review process, consider whether any changes in circumstances necessitate adjusting insurance policies such as life insurance or disability coverage.

Performing a net worth calculation during each review can provide valuable insights into your overall financial health. Comparing net worth over time allows you to gauge progress by identifying increases or decreases in assets and liabilities.

Revisiting your budget during the review stage ensures that it remains realistic and effective in managing expenses while aligning with your financial goals. Assessing income and expenditure patterns enables adjustments that reflect changes in income or spending habits over time.

Regular review of your financial plan is a crucial step in financial planning.

Evaluate your progress, analyze changes in circumstances, manage investments, review insurance coverage, calculate net worth, and reassess budgeting strategies, so you can make necessary adjustments to keep your plan on track and aligned with your evolving goals.

Engaging the expertise of a financial advisor or planner can further enhance the process by providing valuable insights and recommendations based on market trends and financial forecasts. Embracing this ongoing review and revision cycle ensures that you remain proactive in managing your finances while adapting to life’s various twists and turns.

Conclusion on steps in financial planning.

Following the steps in financial planning is crucial for achieving long-term financial health and stability. Through careful debt management, budgeting, and saving, individuals can take control of their finances and work towards a brighter future.

The establishment of an emergency fund is vital to safeguard against unforeseen circumstances and ensure financial resilience.

Moreover, it is essential to regularly review and revise your financial plan to adapt to changing circumstances and goals. This allows for adjusting short-term goals while keeping sight of long-term planning objectives.

By considering factors such as cash flow analysis, net worth calculation, investment strategy, tax planning, and insurance needs, individuals can optimize their wealth management strategies.

Throughout this journey in financial planning steps, it is essential to develop strong financial literacy by educating oneself about various financial instruments and concepts.

Seeking the guidance of a qualified financial advisor can provide valuable insights tailored to individual circumstances and help navigate complex decisions. By implementing these steps diligently, individuals can create a solid foundation for their personal finance journey.

Furthermore, they will be equipped with the necessary tools to make informed decisions about budgeting effectively, saving consistently for short- and long-term goals such as retirement savings or other aspirations. Ultimately, while the path towards financial stability may require discipline and patience at times, it also presents an opportunity for personal growth and empowerment.

By taking ownership of our finances through comprehensive financial planning steps, we are paving the way towards a more secure future filled with endless possibilities.

Remember that every journey starts with a single step! Take that step today towards your own prosperous future by embracing the principles of effective financial planning!

FAQ about steps in financial planning.

A word of encouragement to learn about steps in financial planning.

Embracing the journey of financial planning can be transformative. Imagine it not just as a pathway to wealth, but as a tool to craft the life you deserve. Every step you take, no matter how small, brings clarity and empowerment.

The knowledge you gain today can be the shield against life’s uncertainties and the ladder to your loftiest dreams. Your dedication to understanding and implementing these steps holds the promise of a brighter, more secure future.

Dive in with enthusiasm and belief, for every informed decision you make today will echo as a victory in the chapters of your life ahead!

Przemo Bania is a blogger and writer who helps people get out of their traditional jobs to start a blogging career. Przemo also runs a health blog advocating for endometriosis and fibromyalgia…